Maharashtra Crop Insurance Premiums 45% Higher Than Payouts in 8 Years: PMFBY Analysis

Maharashtra Crop Insurance Premiums 45% Higher Than Payouts in 8 Years

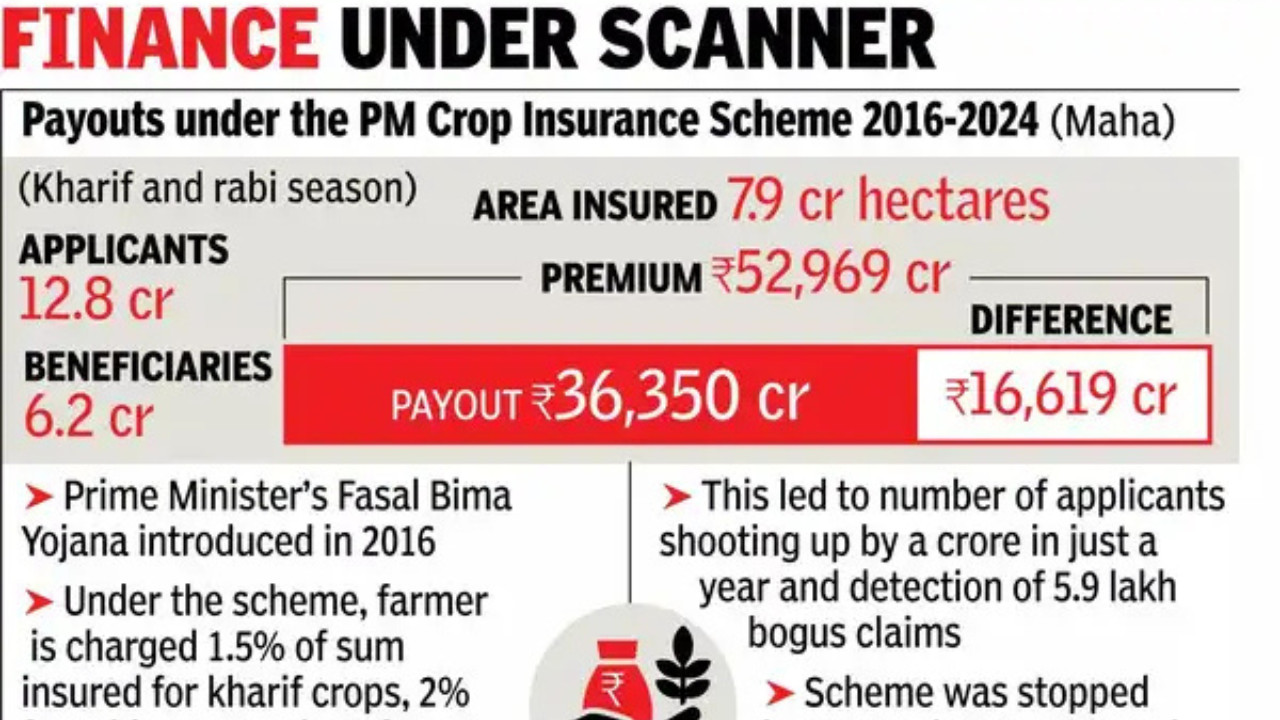

Maharashtra Crop Insurance Premiums 45% Higher Than Payouts in 8 Years: Between 2016-17 and 2023-24, the state of Maharashtra witnessed an alarming trend in its agricultural insurance statistics. Despite enduring multiple climate-induced calamities such as droughts, floods, and unseasonal rains, the total insurance premiums paid to companies under the Pradhan Mantri Fasal Bima Yojana (PMFBY) amounted to ₹52,969 crore. Shockingly, the total payout made to farmers during the same period was only ₹36,350 crore — a stark 45% lower than the premiums collected.

According to data presented at a government review meeting, only 6.2 crore out of 12.8 crore farmers who applied for the scheme received any compensation. This has raised serious concerns about the effectiveness and transparency of PMFBY implementation in the state. The imbalance in premiums and payouts highlights the financial burden on farmers who, in many cases, are left without adequate relief even after paying premiums regularly.

Officials argue that the insurance model operates on risk pooling, and in years of good rainfall and yield, payouts naturally remain low. However, farmer rights groups and agriculture activists question the value proposition of a scheme where half the applicants do not receive any benefits, especially when they are struggling to recover from crop losses. This brings the spotlight back on the efficiency, accountability, and need for reform in PMFBY.

PM Fasal Bima Yojana (PMFBY): An Overview

Launched in 2016, the Pradhan Mantri Fasal Bima Yojana (PMFBY) aims to provide financial support to farmers in case of crop failure due to natural calamities. While the scheme is implemented by both state and central governments, it is executed through empanelled insurance companies.

Who Can Apply?

- All farmers growing notified crops in notified areas during the season.

- Loanee farmers (with crop loans) are compulsorily covered.

- Non-loanee farmers (without crop loans) can apply voluntarily.

- Applicable for both Kharif and Rabi seasons.

- Farmers with land ownership or cultivation rights can apply.

- Tenant and sharecropper farmers are also eligible, with valid documents.

Also read: How Indians Are Paying Insurance Premiums in 2025: UPI, Credit Cards, and Monthly Plans Lead the Way

Insurance Premium Rates

| Crop Season | Crop Type | Farmer’s Premium Share |

|---|---|---|

| Kharif | Food & Oilseeds | 2% of Sum Insured |

| Rabi | Food & Oilseeds | 1.5% of Sum Insured |

| Annual | Commercial Crops | 5% of Sum Insured |

How Does It Work?

- Farmers pay a nominal premium based on crop and season.

- Insurance covers loss due to natural disasters, unseasonal rains, pests, and disease outbreaks.

- In case of crop loss, compensation is assessed through on-ground surveys and remote sensing technology.

- Insurance payout is credited directly to the farmer’s bank account.

Benefits of PMFBY

- Timely financial assistance to cover losses.

- Encourages farmers to adopt innovative farming practices.

- Promotes credit discipline by protecting loanee farmers.

- Acts as a social safety net during unpredictable weather events.

- Builds confidence among rural farming communities.

How to Apply for PMFBY?

Online Application Process

- Visit https://pmfby.gov.in/

- Click on “Apply Online”.

- Register with your Aadhaar number and mobile number.

- Select your state, district, and crop details.

- Upload required documents:

- Aadhaar Card

- Land ownership/cultivation certificate

- Bank passbook (for account details)

- Passport-sized photo

- Submit the application and download the receipt.

Offline Application

- Visit your nearest bank branch, common service centre (CSC), or agriculture office.

- Submit your documents along with the insurance premium.

- Collect the acknowledgment receipt.

Important Dates

| Season | Application Start Date | Last Date to Apply |

|---|---|---|

| Kharif | April 1 | July 31 |

| Rabi | October 1 | December 31 |

Disclaimer

This article is for informational purposes only. Readers are advised to visit the official PMFBY website or consult their local agricultural office for the most accurate and updated information. The government periodically revises rules, premium rates, and guidelines under the scheme.

Maharashtra Crop Insurance Premiums 45% Higher Than Payouts in 8 Years Conclusion

The 45% gap between premiums and payouts in Maharashtra raises serious questions about the viability and farmer-centric approach of PMFBY. With nearly half of all applicants not receiving compensation, it becomes crucial to ensure more transparency in damage assessment, faster claim processing, and direct accountability of insurance companies.

While the scheme has successfully insured crores of farmers, there is room for improvement in execution, grievance redressal, and coverage of marginal farmers. Better monitoring mechanisms and use of real-time technologies like satellite imaging can bridge gaps in damage verification and improve claim satisfaction.

It’s also important to consider customizing premiums based on region-specific risks instead of a one-size-fits-all model. Farmers in areas prone to climate disasters should receive greater protection and quicker disbursement of claims.

As climate change continues to impact agriculture unpredictably, schemes like PMFBY need to evolve rapidly, ensuring no farmer is left behind. Only then can India achieve its goal of financially empowered, climate-resilient agriculture.

Maharashtra Crop Insurance Premiums 45% Higher Than Payouts in 8 Years FAQs

1. Why is the insurance payout in Maharashtra lower than the premium collected?

The insurance payout is lower primarily because insurance works on risk pooling. In years where there is less damage, the collected premium is not returned but retained for future use or profit. Also, inefficient claim verification, bureaucratic delays, and technical rejections may contribute to fewer payouts.

2. How can a non-loanee farmer apply for PMFBY?

Non-loanee farmers can apply by visiting the official PMFBY portal or through nearby Common Service Centres (CSCs). They need to provide Aadhaar, land documents, bank details, and pay the prescribed premium for their crop and season.

3. What happens if a farmer’s claim is rejected?

If a claim is rejected, farmers can approach the district grievance redressal committee, appeal through offline channels or submit complaints on the PMFBY portal. However, outcomes depend on evidence submitted, damage survey data, and policy compliance.

4. Are all crops covered under PMFBY?

No. Only notified crops in each state/district are eligible for coverage. Typically, these include food grains, oilseeds, and some commercial crops. The list changes every season and is notified by the state government in advance.

5. Is PMFBY mandatory for all farmers?

PMFBY is mandatory only for loanee farmers—those who have taken seasonal crop loans. For non-loanee farmers, participation is voluntary, but highly recommended to safeguard against potential crop losses.

Related Posts :

Share This Post